As president of KBD, Curtis aims to simplify insurance for his clients. He’s helped lead KBD to become one of Canada’s fastest 400 growing companies according to the Globe & Mail.

Published on:

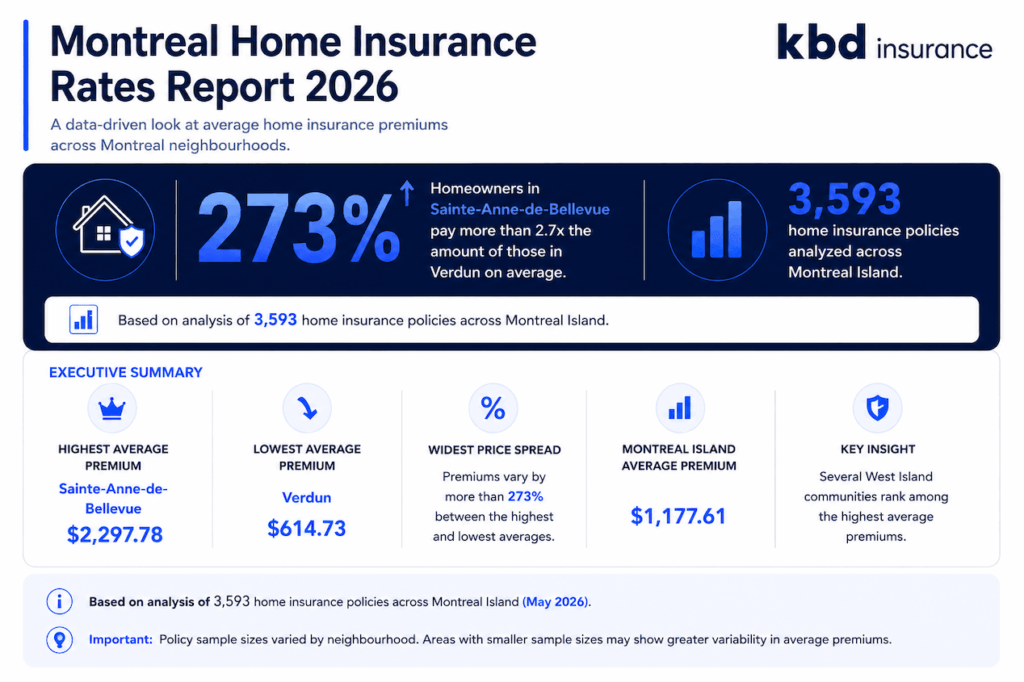

An analysis of original anonymized home insurance policy data covering 3,593 policies revealed significant differences in average annual home insurance premiums across Montreal neighbourhoods and municipalities.

Published: June 2026

Prepared by: KBD Insurance

Dataset: 3,593 analyzed home insurance policies across Montreal Island

KBD Insurance reviewed anonymized home insurance premium data from municipalities and neighbourhoods across Montreal Island. The analysis identified substantial geographic differences in average home insurance pricing across the region.

This report analyzes average premiums by postal-region-level geography. Because home insurance pricing is influenced by many factors – including rebuilding costs, property characteristics, claims exposure, weather-related risk, and coverage selections – the report does not attribute premium differences to any single factor or underwriting variable.

Disclaimer: Some neighbourhoods included smaller policy sample sizes than others, which may increase variability in average premiums. The premiums shown in this report represent averages and may not reflect the cost of individual home insurance policies.

In this report, you’ll find:

- Why this analysis matters for Montreal homeowners

- An overview of home insurance premiums across Montreal

- Key takeaways from the dataset

- Table of home insurance cost differences across Montreal Island

- The top 11 most expensive areas for home insurance

- The top 11 least expensive areas for home insurance

- Borough & neighbourhood comparisons across Montreal

- Why home insurance costs vary across Montreal neighbourhoods

- Broader Quebec & Canadian home insurance trends

- Montreal vs. Quebec average home insurance rates

- What the data means for homeowners

- What the data means for insurance professionals

- How home insurance premiums may change over time

- Methodology, sources & citations

- Conclusion

Why this analysis matters for Montreal homeowners

Montreal homeowners may not realize how significantly home insurance premiums vary depending on where in the city they live.

As insurers increasingly rely on localized underwriting models and granular geographic data, they are able to price risk at increasingly precise geographic levels, in addition to traditionally referenced postal codes.

By understanding localized insurance trends, Montreal homeowners can better evaluate coverage needs, anticipate potential insurance costs, and recognize how broader market conditions may influence premiums over time.

An overview of home insurance premiums across Montreal

A data-informed overview of average home insurance premiums across Montreal municipalities and neighbourhoods.

Important: Policy sample sizes varied by neighbourhood. Areas with smaller sample sizes may show greater variability in average premiums.

The analysis found significant geographic differences in average home insurance premiums across Montreal Island, with the region-wide average premium reaching $1,177.61 across 3,593 analyzed policies.

While some municipalities reported average premiums well below the island average, others (particularly several West Island communities) showed substantially higher costs, highlighting how dramatically home insurance pricing can vary depending on location.

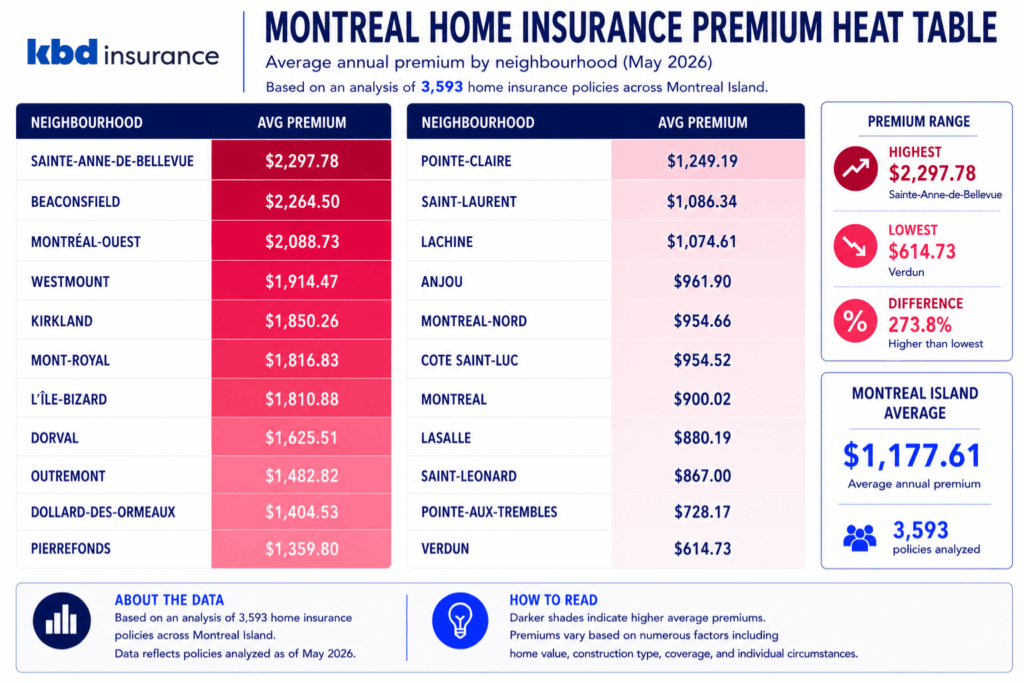

Home insurance premiums by neighbourhood

The dataset revealed substantial differences in average home insurance premiums across Montreal neighbourhoods and municipalities, with premiums ranging from $614.73 in Verdun to more than $2,297 in Sainte-Anne-de-Bellevue.

Key takeaways from the dataset

- 3,593 home insurance policies analyzed: The report analyzed anonymized policy-level data across Montreal Island to identify neighbourhood-level differences in average home insurance premiums.

- Sainte-Anne-de-Bellevue reported the highest average premium: Sainte-Anne-de-Bellevue reported the highest average annual premium in the dataset at $2,297.78, based on 73 analyzed policies.

- Verdun reported the lowest average premium: Verdun reported the lowest average annual premium at $614.73, based on 149 analyzed policies.

- Premiums varied by more than 270% across municipalities: The difference between the highest and lowest average premiums exceeded 270%, highlighting how dramatically home insurance pricing can vary geographically across Montreal.

- Several West Island communities ranked among the highest premiums: Communities including Beaconsfield, Kirkland, Dorval, and Sainte-Anne-de-Bellevue reported some of the highest average premiums in the dataset.

- The Montreal category reported an average below the island-wide average: The Montreal category reported an average premium of $900.02, below the Montreal Island average of $1,177.61.

- Smaller municipalities showed greater variability in average premiums: Some municipalities included smaller policy sample sizes than others, which may contribute to greater variability in premium averages across certain regions.

Table of home insurance cost differences across Montreal

This table highlights significant geographic differences in average home insurance premiums across Montreal. Municipalities such as Verdun and Pointe-aux-Trembles reported substantially lower average premiums than the Montreal Island average.

The geographic distribution of premiums demonstrates that home insurance costs are not uniform across Montreal Island. Even neighbouring municipalities can report markedly different average premiums.

Important: Policy sample sizes varied by neighbourhood. Areas with smaller sample sizes may show greater variability in average premiums.

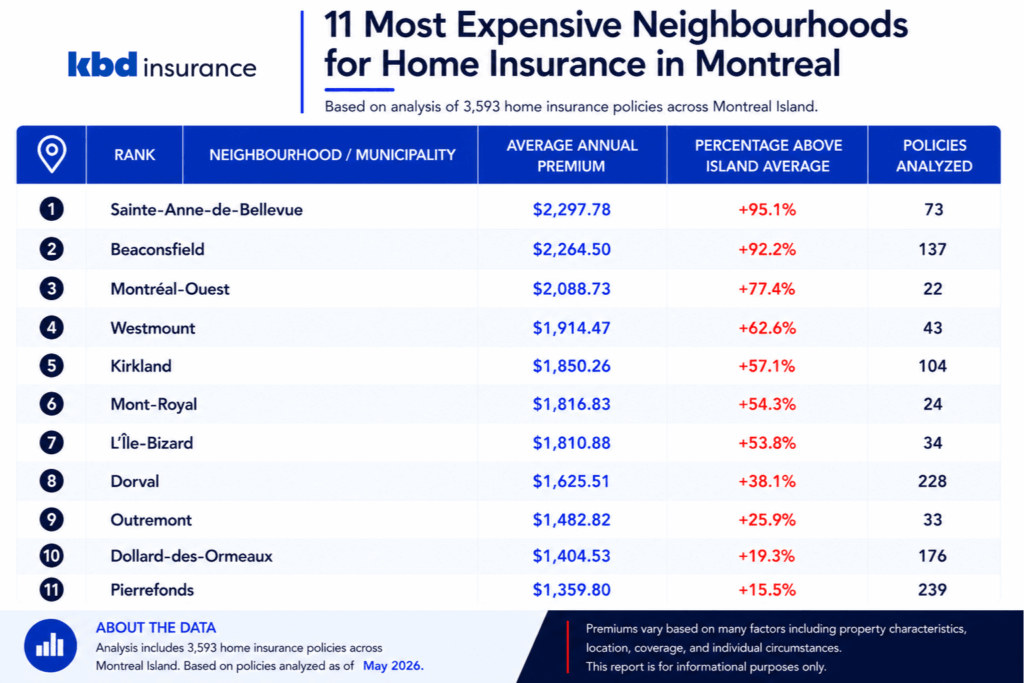

The top 11 most expensive areas for home insurance in Montreal

The top 11 most expensive areas for home insurance reported average annual premiums ranging from $1,359.80 to $2,297.78, representing 15.5% to 95.1% above the Montreal Island average of $1,177.61.

Several West Island municipalities ranked among the highest-premium communities in the dataset, including Sainte-Anne-de-Bellevue, Beaconsfield, Kirkland, Dorval, and Dollard-des-Ormeaux.

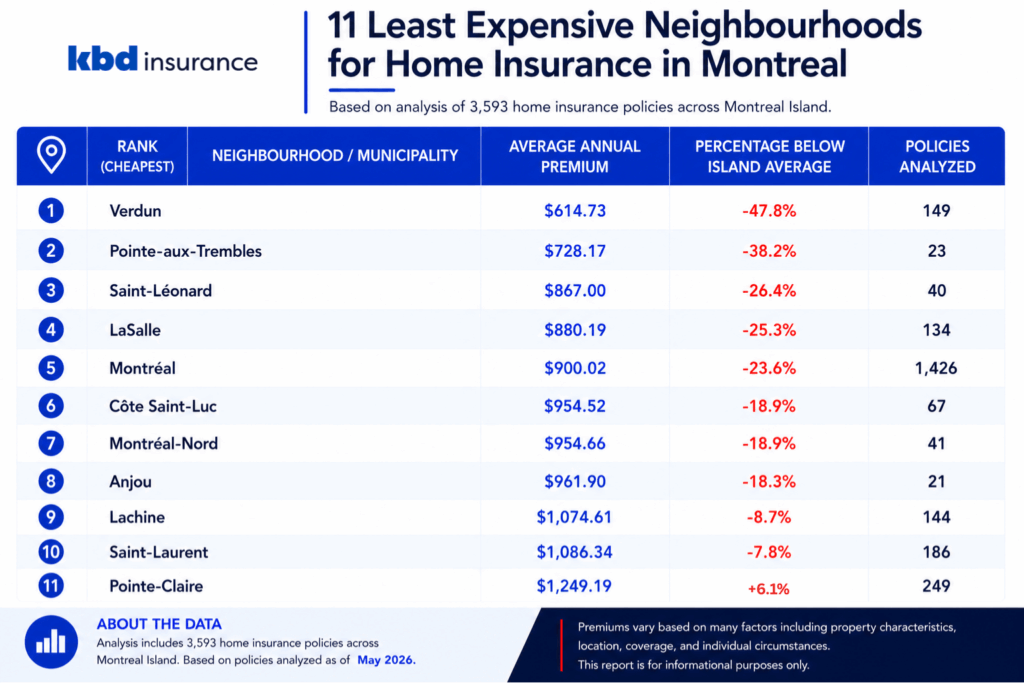

The top 11 least expensive areas for home insurance in Montreal

The 11 least expensive areas for home insurance reported average annual premiums ranging from $614.73 to $1,249.19. Relative to the Montreal Island average of $1,177.61, premiums ranged from 47.8% below to 6.1% above the island-wide average.

Based on 2,480 analyzed policies, Verdun reported the lowest average premium in the dataset, followed by Pointe-aux-Trembles and Saint-Léonard.

Borough & neighbourhood comparisons across Montreal

Several West Island municipalities reported some of the highest average home insurance premiums in the dataset, including Sainte-Anne-de-Bellevue, Beaconsfield, Kirkland, and Montreal-Ouest.

Interestingly, this represented a reversal from KBD Insurance’s separate auto insurance analysis, where several West Island communities reported comparatively lower average auto insurance premiums.

The Montreal category reported an average premium of $900.02 – well below the Montreal Island average of $1,177.61 – despite representing the largest policy sample in the analysis, with 1,426 policies.

Several urban-core and eastern municipalities, including Verdun, Pointe-aux-Trembles, and LaSalle, reported some of the lowest average home insurance premiums across the dataset.

The contrast with the auto insurance findings highlights how home insurance and auto insurance are evaluated using different underwriting considerations. Home insurance pricing places greater emphasis on factors such as rebuilding costs, property characteristics, water damage exposure, and localized risk patterns.

Why home insurance costs vary across Montreal neighbourhoods

Factors that influence home insurance costs

Home insurance premiums in Canada can be influenced by a wide range of property-specific, geographic, and environmental considerations. While pricing varies between insurers and policies, underwriting models increasingly rely on localized data to help evaluate regional claims exposure, rebuilding risk, and broader property-related trends across different communities.

Below are common factors that influence home insurance premiums:

- Rebuilding costs: Areas with higher construction, labour, and material costs may experience higher estimated rebuilding expenses following a claim.

- Property values: Higher-value homes often require greater replacement coverage which can contribute to higher average premiums.

- Housing age: Older homes may present different underwriting considerations related to plumbing, wiring, roofing, and overall property condition.

- Water damage exposure: Water damage remains one of the most common and costly home insurance claim types across Canada.

- Sewer backup risk: Neighbourhood infrastructure, drainage systems, and flood exposure may influence sewer backup-related claims risk.

- Flood exposure: Areas with greater flood or overland water exposure may face different underwriting considerations and coverage requirements.

- Fire protection access: Proximity to fire stations, hydrants, and emergency services can influence property risk assessments.

- Weather & climate exposure: Severe weather events, storms, and climate-related claims continue affecting home insurance markets across Canada.

- Claims history: Regional claims trends and historical loss patterns may contribute to localized pricing differences.

- Crime & vandalism exposure: Rates of vandalism, break-ins, and property-related crime may vary geographically and can affect insurance pricing.

- Localized catastrophe modeling: Insurers increasingly use granular geographic data and catastrophe modeling to evaluate localized environmental and claims exposure risks.

Why postal codes matter in home insurance underwriting

Insurers often use postal-code-level data to help evaluate localized property and environmental risks within home insurance underwriting models. Geographic areas may experience different levels of flood exposure, weather-related claims, rebuilding costs, and historical claims activity, all of which can influence insurance pricing.

While postal code is only one factor considered within underwriting, the data highlights how nearby Montreal communities can still report substantially different average home insurance premiums.

Broader Quebec & Canadian home insurance trends

Home insurance costs across Quebec and Canada have risen due to mounting catastrophe losses, severe weather events, and increasing rebuilding costs. Water damage remains the most common claim type in Quebec, with sewer backups and overland flooding exacerbated by aging infrastructure and extreme rainfall – particularly relevant to Montreal’s older urban neighborhoods.

At the same time, construction inflation, rising labour costs, and skilled trade shortages continue driving up rebuilding and replacement values. Quebec home insurance premiums reportedly rose 10.1% in Q2 2025, above the national average of 6.9%, while KBD data showed the province’s average home insurance premium reached approximately $2,088 annually at the start of 2026.

While these broader market trends are affecting homeowners across the province, neighbourhood-level analysis remains essential for understanding home insurance costs in Montreal. Environmental exposure, property characteristics, and localized risk factors can all contribute to premium differences across the island.

Montreal vs. Quebec average home insurance rates

As of January 2026, KBD data shows that Quebec homeowners paid an average of $2,088 annually for home insurance coverage. In comparison, the Montreal Island average identified in this report was $1,177.61 across 3,593 analyzed policies – approximately 43.6% lower than the broader provincial average.

Because the provincial average reflects a broader mix of property types, coverage selections, insurers, and geographic regions across Quebec, direct comparisons should be interpreted with caution.

What this data means for homeowners

The data highlights how significantly home insurance costs can vary depending on where homeowners live across Montreal Island.

The dataset also reinforces the importance of regularly reviewing home insurance coverage, particularly as rebuilding costs, property values, and climate-related risks continue evolving across Canada.

Homeowners may benefit from reviewing optional protections such as flood and sewer backup endorsements while ensuring coverage limits accurately reflect current rebuilding and replacement values.

What this data means for insurance professionals

The data highlights how geographic risk factors can contribute to pricing differences across communities within Montreal’s home insurance market.

As insurers continue responding to rising climate-related claims, catastrophe exposure, and evolving property risks, underwriting models may increasingly rely on granular geographic data and predictive risk modeling to support pricing accuracy.

The findings demonstrate how localized risk assessment continues shaping home insurance pricing outcomes at the neighbourhood level.

How home insurance premiums may change over time

Home insurance premiums across Canada may continue evolving as insurers respond to rising climate-related claims, severe weather events, and increasing rebuilding costs. Flooding, water damage, windstorms, and other catastrophic weather-related losses have become increasingly important considerations within the home insurance market.

At the same time, inflation, construction labour shortages, and rising material costs may continue affecting rebuilding and replacement values for homeowners. As environmental and economic pressures evolve, home insurance premiums may continue changing across different regions and communities.

Methodology

Data & geographic scope

This analysis is based on anonymized home insurance policy data from KBD Insurance. The report analyzed 3,593 home insurance policies across Montreal Island and focused on average annual premiums grouped by neighbourhood and postal-region-level geography.

Timeframe analyzed

The report reflects policy data current as of May 2026.

Limitations & important considerations

Some municipalities included smaller policy sample sizes than others, which may increase variability in average premiums. Home insurance pricing is influenced by many variables beyond geography alone, including property characteristics, rebuilding costs, claims history, coverage selections, housing age, and localized environmental exposure.

This analysis does not include every neighbourhood and municipality on the Island of Montreal. Findings are based solely on locations with sufficient insurance policy data available for analysis.

This report is intended for informational purposes only and does not attribute premium differences to any single factor or underwriting variable.

Sources & citations

Where applicable, supporting industry context and statistics were referenced from Canadian insurance organizations, government datasets, and publicly available industry reports.

Wrap up: what the analysis means

The analysis highlights how significantly home insurance premiums can vary across Montreal municipalities and neighbourhoods, reinforcing the importance of geographic and property-related risk factors within today’s home insurance market.

About KBD Insurance

KBD Insurance is a local Montreal insurance brokerage with 40+ years of experience serving individuals and businesses across the province. The firm provides insurance solutions across home, auto, commercial, and specialty insurance markets.

For additional information, media inquiries, quotes, or industry insights, contact KBD Insurance at info@kbdinsurance.com.