As president of KBD, Curtis aims to simplify insurance for his clients. He’s helped lead KBD to become one of Canada’s fastest 400 growing companies according to the Globe & Mail.

Edited on:

Published on:

Third party liability insurance provides coverage in the event that you’re found responsible for damages to a third party – whether it’s related to business, auto, or home.

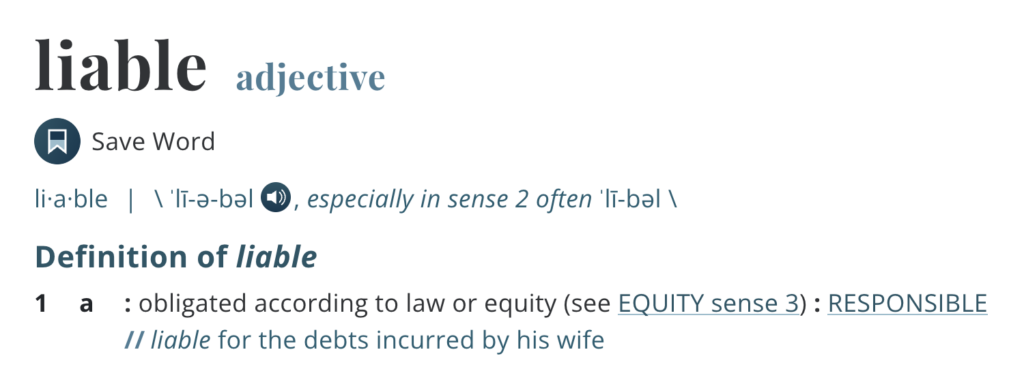

Liability is a word people throw around a lot, but what does it actually mean?

Let’s start with a little vocab lesson.

Here’s what our friends at Merriam-Webster have to say:

Basically, to be held liable in an insurance claim means that you’re the party being held responsible.

Now that we’ve got that covered, what is liability insurance?

Liability insurance is a baseline coverage that’s automatically included in most insurance policies.

In short, it covers you for claims in which you’re responsible for bodily injury and/or property damage to a third party.

It works this way in Ontario, and Canada-wide.

Below, we’re explaining everything you need to know about third party liability insurance, from what it is, to what it covers, and why you need it.

Don’t feel like reading?

We get it.

Get in touch instead, and we’ll find the best insurance coverage for you.

Jump ahead to learn:

- What is third party liability insurance?

- Why do I need third party liability insurance?

- How much does third party insurance cover?

- What does third party liability insurance not cover?

- What are the benefits of third party liability insurance?

What is third party liability insurance?

Third party insurance protects the insurance client from claims made against them by a third party.

In super simple terms, liability insurance will protect you if someone else tries to sue you because you caused them bodily injury or property damage.

To put this into context, here are the different “parties” that are involved in an insurance claim.

- 1st party = The insurance client (you)

- 2nd party = The insurance company

- 3rd party = Individuals/businesses making a claim against the insurance client (you)

For example, say you’re involved in a car accident in which you’re held liable (aka: responsible).

Remember that little vocab lesson we went over?

If you’re sued for bodily or property damages related to the accident, your third party coverage will kick in.

If this happens, your liability insurance will pay out to the third party, and not to you, the policyholder.

Remember: Liability insurance is a baseline coverage that you’ll see in every kind of insurance policy, from home, to car, to business, and so on.

Because of this, there are several different kinds of liability insurance coverages – depending on the assets you need insured.

For example, the different types of liability insurance include:

- Home liability insurance

- Auto liability insurance

- Commercial liability insurance

- Professional liability insurance

To summarize, liability insurance covers you for legal fees and payouts if you’re found responsible in a claim for damages to a third party.

Make sense? Good.

Now, let’s move on to why you need third party liability insurance in Ontario.

Or you can just give us a call.

Why do I need third party liability insurance in Ontario?

Liability insurance is important because it covers you in situations where you’re found responsible for damages to a third party.

It’s also the law to carry car liability insurance while driving!

Depending on the circumstance, you could be held liable for a huge sum in legal, replacement, and medical expenses.

So, liability insurance pays out for things like:

- Legal fees

- Repairs

- Replacement costs

- Other payouts (medical bills, rehabilitation costs, etc.)

Without liability insurance, you’d be required to pay out of pocket, and most people don’t have the cash on hand to do so.

Which is why being properly insured is so important.

Need home, car, or business insurance?

How much does third party insurance cover?

In general, third party liability insurance has two main components:

- Bodily injury liability coverage

- Property damage liability coverage

However, the minimum amount that you’re required to be covered for depends on the type of insurance you’re getting, and the province you live in.

Let’s take car insurance for example.

Drivers in Ontario have to carry a minimum of 200k in third party liability car insurance, whereas Quebec drivers are only required to carry 50k in liability.

See the difference?

And most drivers opt to be covered for much more than this – because 200k in third party liability often isn’t enough to cover you in an accident involving bodily injury or property damage to others.

Claims like this can easily cost several hundreds of thousands of dollars – especially if they happen outside of your home province or in the USA.

This factor plays into why third party liability is mandatory automobile coverage throughout Canada.

And automobile third party liability insurance covers damages related to:

- Bodily injury

- Property damage

Ready to get insured?

Give the team at KBD a call.

What does third party liability insurance not cover?

Remember, third party liability insurance covers payouts and legal fees for claims made against you by a third party.

Third party liability insurance does not cover your own damages, whether bodily injury or property damage or loss.

Still have questions?

Give us a call.

What are the benefits of third party liability insurance?

Third party liability insurance coverage can be especially beneficial if you have a lot of assets.

Basically, the more you have, the more coverage you’ll need.

The same goes for companies that service or sell products to a large clientele; the bigger your client base, the more chance there is of there being a third party claim.

Think about it: If you run a big business and people are constantly coming in and out, the risk goes up.

In both cases, having the right amount of liability coverage in place is a smart way to protect your personal and business assets.

Need liability coverage?

Give us a call.

Wrap-up

There you have it: Insurance basics 101.

You’re now officially schooled on third party liability insurance.

IQ point earned.

Well done.

Do you still have questions?

Need home, car, or business liability insurance in Ontario?

Give us a call.

Get to know KBD on social media. We’re up to some cool stuff.

YouTube, Instagram, TikTok